the Most Distant Galaxy in the Universe and Breaks Its Own Record")

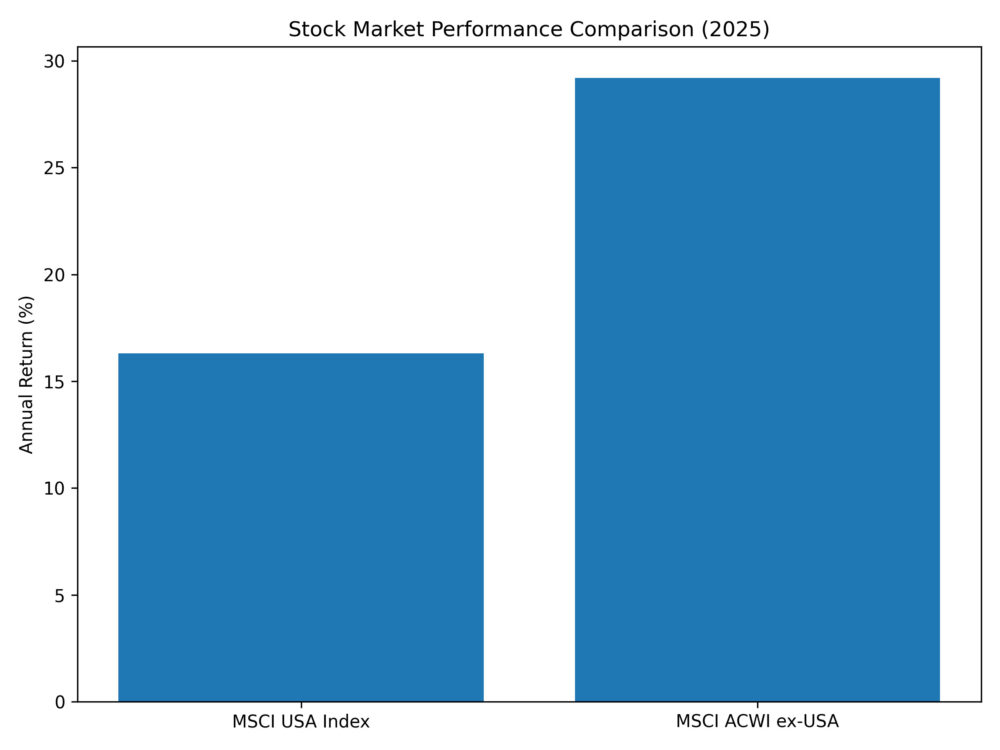

It’s the season when investors check their portfolios to decide whether the holidays call for champagne and caviar or something closer to beer and chips. On paper, the answer seems clear: the MSCI USA Index posted a 16.3% gain, well above its long-term average and marking a third consecutive year of solid stock-market returns.

Yet that headline figure masks a more uncomfortable reality.

Measured against the rest of the world, US markets have been relative underperformers. The **MSCI All Country World Index excluding the United States surged 29.2%, leaving American stocks far behind. Nothing this lopsided has occurred since 2009, when global markets were rebounding unevenly from the financial crisis.

Equities are not the exception. US bonds and the dollar have also lagged global peers, suggesting that investors are broadly reassessing exposure to American assets.

The Disappearance of America’s Economic Premium

This shift comes uncomfortably soon after The Economist dubbed the US economy “the envy of the world.” It also sits uneasily alongside President Donald Trump’s repeated claims that America is the world’s “hottest” economy.

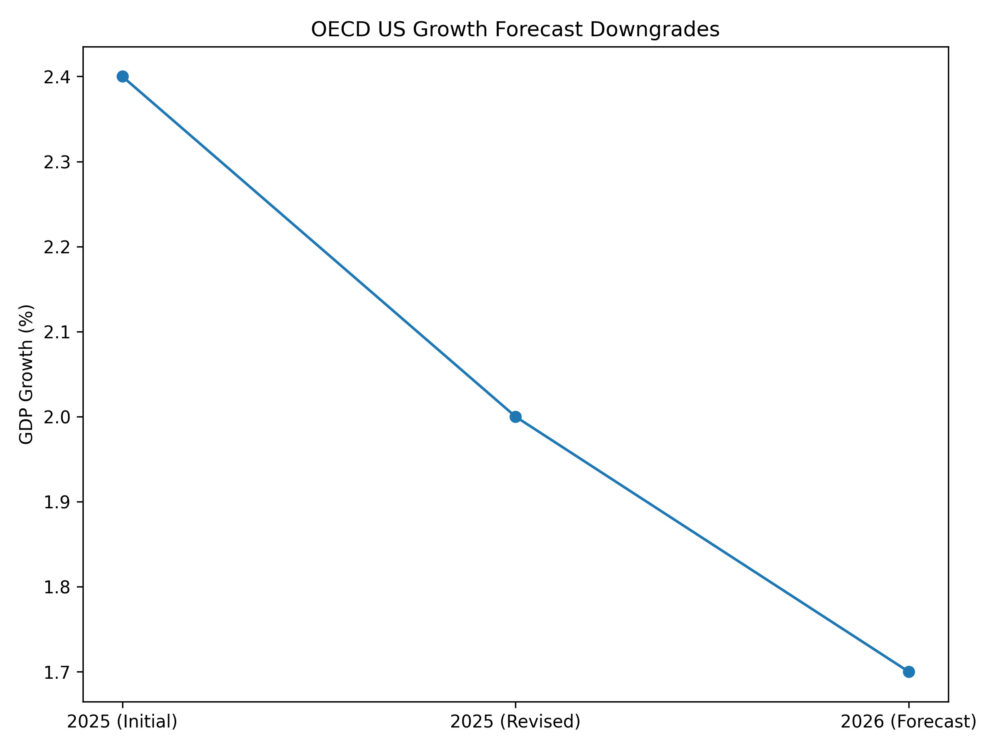

The clearest explanation lies in revised forecasts from the Organisation for Economic Co-operation and Development. At the start of 2025, the Paris-based body projected US growth of 2.4%, comfortably ahead of the 1.9% expected for other advanced economies. That advantage has evaporated.

The OECD now expects US growth of just 2% in 2025, slowing further to 1.7% in 2026 — exactly in line with the broader OECD average. America’s growth premium is gone.

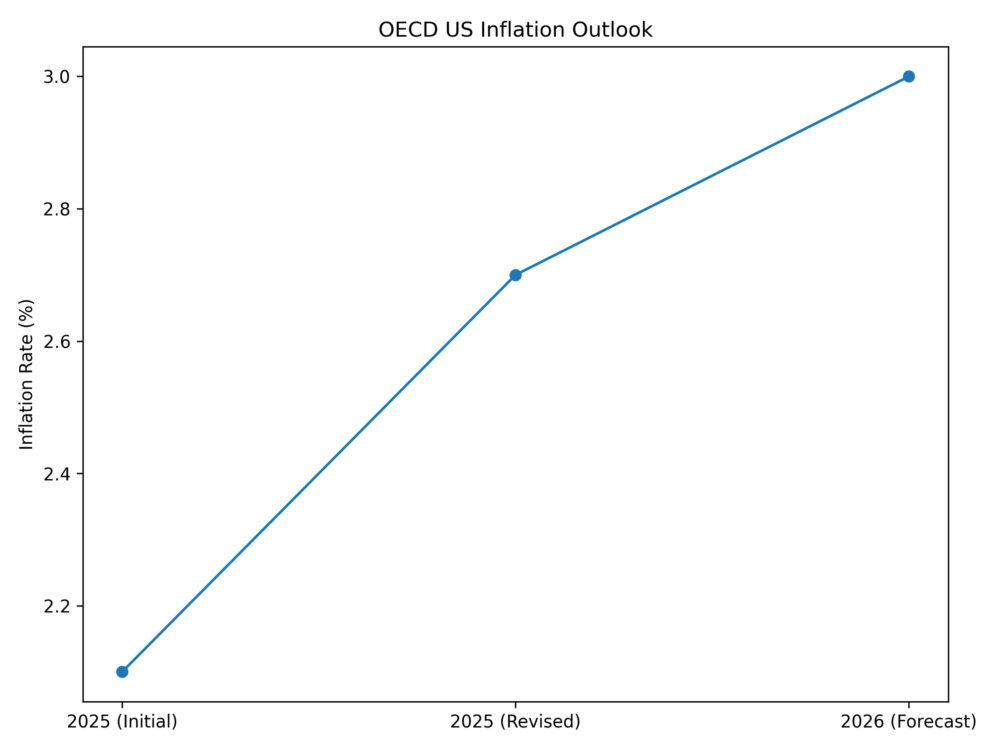

Inflation tells a similar story. As 2024 ended, the OECD projected a benign 2.1% inflation rate for 2025. That optimism has faded. The organisation now estimates inflation reached 2.7% in 2025 and could rise to 3% in 2026.

In short, the macroeconomic case for US exceptionalism has weakened materially.

Policy Chaos and Investor Fatigue

Markets can tolerate bad news. What they struggle with is unpredictability. Across trade, tariffs, foreign policy, healthcare, immigration, national security, education, and energy, the Trump administration has injected persistent uncertainty into decision-making for businesses and households alike.

Tariffs — effectively a tax on imports and consumption — sit at the core of the administration’s economic agenda. Combined with erratic messaging and confrontational politics, they have undermined confidence. The idea that electing a self-described “businessman” would bring stability increasingly looks misplaced.

Strong GDP, Fragile Foundations

Supporters point to headline data, including a 4.3% annualised expansion in third-quarter GDP, beating economists’ expectations. But the internals tell a more troubling story.

Growth was driven by a 3.5% surge in personal consumption, even as real disposable income remained flat. Households are spending not because they’re earning more, but because they’re drawing down savings.

That behaviour is visible in the data. The personal saving rate has fallen to 4%, its lowest level since 2022, when inflation was surging. History suggests such dynamics are unsustainable.

Businesses Are Pulling Back

For companies, the policy environment has made planning difficult. A recent survey by Duke University and the Federal Reserve Bank of Richmond shows chief financial officers are no more optimistic about the economy than they were in early 2020, at the height of pandemic fears.

Small businesses — the backbone of US job creation — are already reacting. According to the November ADP National Employment Report, private employers with fewer than 50 workers cut 120,000 jobs, the largest one-month decline since May 2020.

Corporate earnings among publicly listed firms remain strong, but that strength is not shared broadly. National income data analysed by JPMorgan Chase & Co. show a 5.6% contraction in profits over the year through June.

The stress is visible in bankruptcy filings as well. At least 717 companies filed for bankruptcy in 2025 through November, the highest number since 2010, according to data cited by The Washington Post.

Consumers Are Losing Confidence

Unsurprisingly, households are growing anxious. The Conference Board’s consumer confidence index has fallen to levels last seen in the early months of the Covid-19 pandemic.

According to the Conference Board’s chief economist, consumer concerns are increasingly dominated by prices, inflation, tariffs, trade policy, and political uncertainty, including fears of a federal government shutdown.

Bonds and the Dollar Signal Deeper Trouble

In fixed income, US assets have also disappointed. Despite the Federal Reserve cutting rates three times since mid-September, long-term Treasury yields rose as investors demanded greater compensation for inflation and fiscal risk.

As a result, the Bloomberg US Aggregate Index returned 7.30% in 2025, trailing the Bloomberg Global Aggregate Index, which gained 8.17%.

One red flag is the surge in the 10-year Treasury term premium, which jumped to 0.91 percentage point after Trump’s April “Liberation Day” tariff announcement — the highest since 2014 — and has remained elevated. Investors are demanding more to lend to Washington.

At the same time, foreign official holders — central banks and sovereign wealth funds — are steadily reducing exposure. Official holdings of US Treasuries have fallen to about 13% of marketable debt, down from 33% a decade ago and nearly 40% fifteen years ago. Fewer lenders typically mean higher borrowing costs for governments, businesses, and households.

The Dollar Votes No Confidence

Currencies often offer the clearest signal of investor sentiment. On that front, the message is stark. The Bloomberg Dollar Spot Index fell nearly 8% in 2025 — its worst performance since 2017, Trump’s first year in office.

The dollar weakened against all 16 of the world’s most-traded currencies, a rare and telling rebuke. While a weaker currency can help exports, it also fuels inflation by raising import costs. Indeed, exports rose 4.7% through September to $1.62 trillion, but imports jumped 7.4% to $2.60 trillion, according to the Bureau of Economic Analysis.

Fool’s Gold, Not a Golden Age

Senior administration officials, including Treasury Secretary Scott Bessent and Commerce Secretary Howard Lutnick, have repeatedly pushed back the timeline for economic prosperity — from confidently “2025” to vaguely “2026.”

For investors and households alike, patience is wearing thin. What was sold as a new “Golden Age” increasingly resembles fool’s gold — shiny on the surface, but lacking the substance needed to sustain confidence at home or abroad.

The markets, it seems, have already made up their minds.